Understanding Multi-Currency Accounts

Why Multi-Currency Accounts Matter for Digital Nomads

For the modern digital nomad, location independence is only half the story. The other half is financial independence — the ability to receive, hold, convert and spend money in multiple currencies with minimal friction. When you’re freelancing from Bali one month, consulting from Lisbon the next and collaborating with clients in Mumbai or New York, traditional single-currency bank accounts often fall short: high conversion fees, slow transfers, local banking limitations and hidden charges.

At Get Founds Technologies we believe that building a thriving digital nomad community means equipping members not just with travel tips and networking events, but with financial tools and literacy to scale their remote careers. A multi-currency account is one of those foundational tools. In this guide, we compare three of the top platforms:

- Wise (formerly TransferWise)

- Revolut

- Payoneer

We’ll break down what they offer, where they excel, what to watch out for, and how to choose the right one (or more than one) as part of your digital-nomad career toolkit.

What Digital Nomads Should Look for in a Multi-Currency Account

Before diving into each product, here are the key features you should prioritise:

- Ability to hold multiple currencies (USD, EUR, GBP, AUD, etc.)

- Ability to receive payments in foreign currencies and convert them at fair rates

- Transparent and low currency conversion / cross-border transfer fees

- Local bank details (IBAN, routing numbers) for major markets so clients can pay you like a local

- Mobile app + debit card with global ATM / point-of-sale access

- Availability across multiple countries / jurisdictions (important for nomads)

- Clear compliance, regulatory standing and good user reviews (you don’t want surprises)

- An account that supports remote onboarding (no need for a physical branch)

- Good integration with your freelance / remote-business tools (invoicing, payouts)

Selecting a multi-currency account is not about “which is perfect” but “which fits your model of — where you earn, what currencies you deal with, and how you travel or settle”.

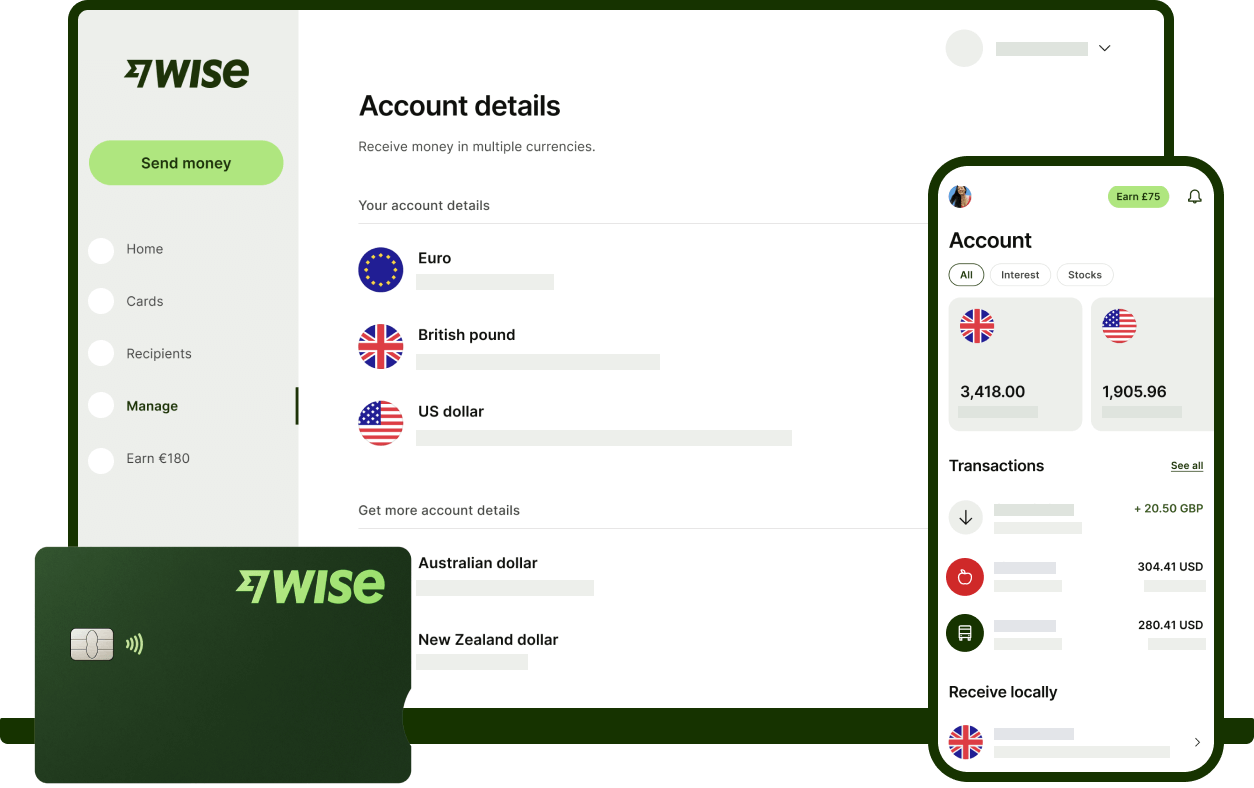

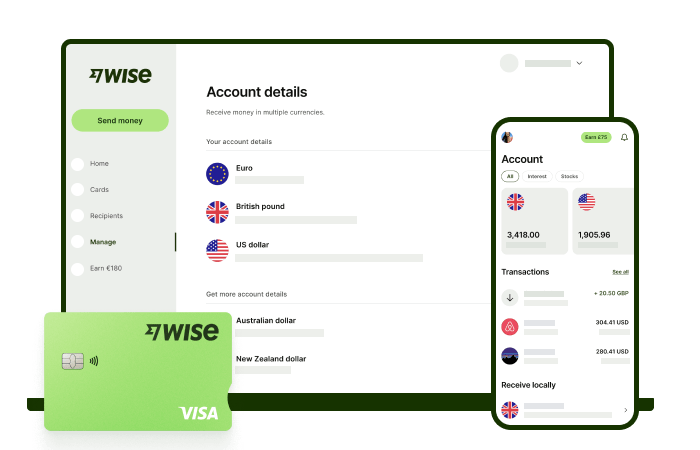

1. Wise – The Transparent Multi-Currency Specialist

Key Features

- Allows you to hold, convert and transfer 40+ currencies in one account.

- Provides local bank account details in major currencies (USD, EUR, GBP, AUD) so you can receive payments as if you had a local bank there.

- Transparent fee structure: conversion uses mid-market rate with a clearly disclosed fee.

- Great for freelancers and digital nomads who receive payments in one currency and spend in another (e.g., get USD but live in Thailand or Portugal).

- Remote onboarding, mobile-first, travel friendly.

Benefits for Digital Nomads

- You can get paid by clients globally into your USD or EUR “local” details, avoiding SWIFT bank fees.

- When you travel or move country, your banking remains stable (same account).

- Lower hidden conversion fees than many banks or other platforms.

- Fits nicely into the nomad mindset of “set it up once, use it anywhere”.

Considerations / Limitations

- While very strong for transfers and multi-currency holding, it might not offer full “banking features” (loans, full-service branches) compared to some digital-banks.

- Some countries may have eligibility restrictions or limited card access. Always check for your home country or residence.

- If you earn via marketplaces that expect a “merchant account” with local payout methods, the platform might differ.

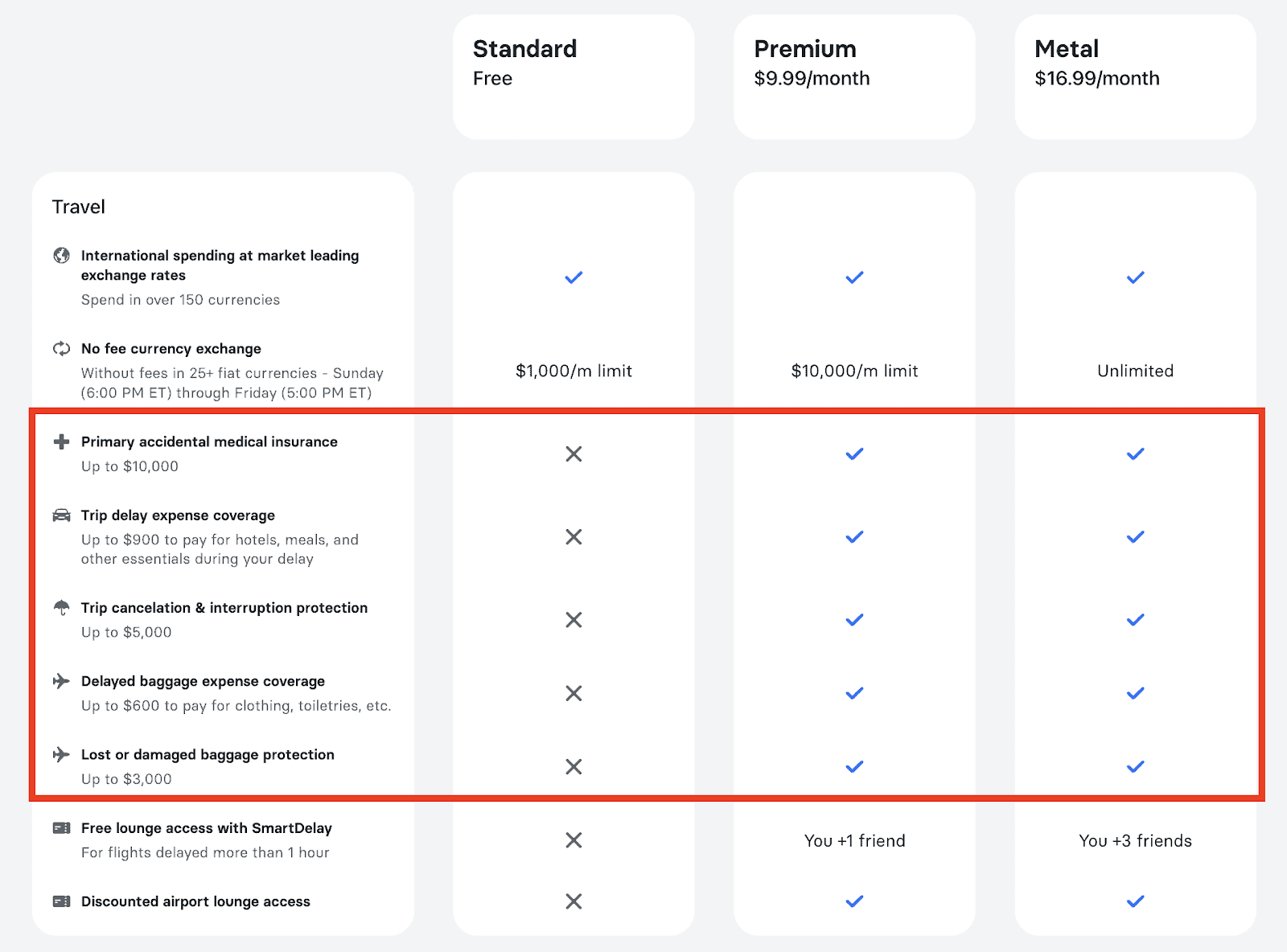

2. Revolut – The Feature-Rich Digital Bank with Multi-Currency Powers

Key Features

- Multi-currency account that allows you to hold and exchange dozens of currencies within the app.

- Additional benefits such as travel-cards, international ATM withdrawals (with plan limits), budgeting tools, travel insurance (on higher tiers) — all appealing for nomad lifestyle.

- Strong global brand, large user base and rapidly expanding presence.

Benefits for Digital Nomads

- If you travel frequently and switch locations/currencies often, Revolut offers convenience and travel-oriented perks.

- The built-in wallet + card means you can hold the currency you need before you travel and minimize conversion surprises.

- Good alternative or companion account to your primary bank.

Considerations / Limitations

- Free tier may limit features (withdrawals, conversions) and you may need paid plan to unlock best benefits.

- Some reports suggest service availability limitations depending on country of residence.

- While feature-rich, the “best exchange rates/lowest fees” may not always beat specialist platforms like Wise.

- Risk: Some users have reported account issues, especially with compliance / money-laundering controls (important for nomads to keep documentation crisp).

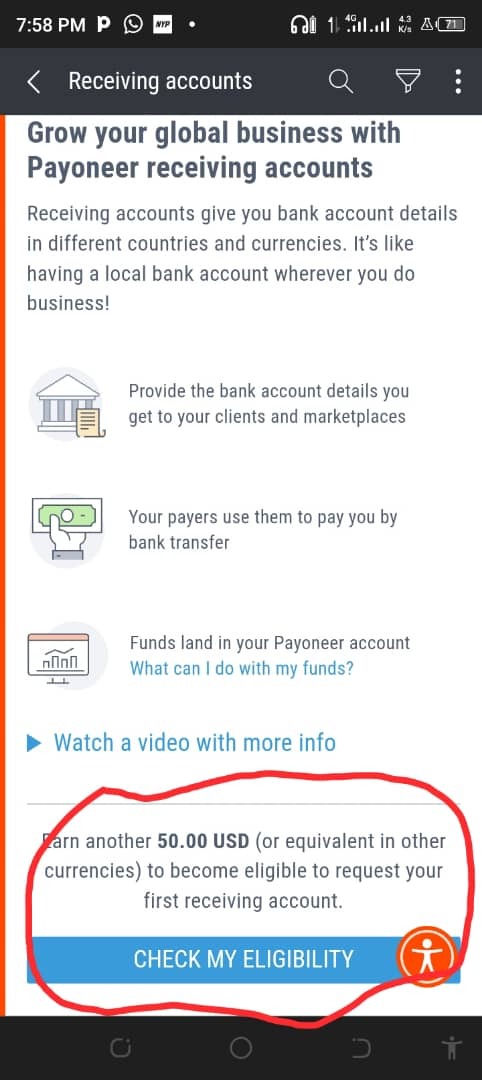

3. Payoneer – The Freelancer / Marketplace Specialist

Key Features

- Designed for freelancers, e-commerce sellers and remote professionals to receive payments globally (USD, EUR, GBP, CAD, AUD etc) via local receiving accounts, even if you don’t live in those regions.

- Supports a wide range of payout sources including marketplaces (e.g., Upwork, Fiverr, e-commerce platforms) and global clients.

- Offers virtual bank details + debit card for spending or withdrawing funds to your local bank account.

Benefits for Digital Nomads

- If your income is heavily tied to online platforms, international clients or you’re selling products/services globally — Payoneer can streamline receiving payments without requiring clients to initiate expensive international bank transfers.

- Helps avoid currency conversion surprises by receiving in target currencies.

- Useful companion account for niche use-case (marketplaces + remote freelance work) alongside your primary banking.

Considerations / Limitations

- Fees can be higher in some flows (withdrawals, non-platform payments) than specialist platforms.

- Not always optimized for spending the funds while living abroad (you may still incur conversions or local bank withdrawal fees).

- For pure travel spending and holding currencies, may not beat Wise/Revolut on cost.

- As with any global provider, check eligibility, supported country of residence, and plan carefully for taxation/legal compliance.

4. Side-by-Side Comparison: Which Suits You?

| Feature | Wise | Revolut | Payoneer |

| Multi-currency holding (many currencies) | ✅ Strong (Exiap) | ✅ Good, but may require paid plan (WiFi Tribe) | ✅ Limited to main currencies but focused on receiving flows (Nomad Gate) |

| Local bank details (USD/EUR/GBP) | ✅ Yes, good support (Wise) | ✅ Some support, depending on region | ✅ Strong: designed for local receiving accounts (Wise) |

| Best for spending/travelling abroad | ✅ Good | ✅ Excellent travel-oriented perks | ⚠️ Less focus on travel perks |

| Best for receiving marketplace/international freelance payments | ✅ Good | ⚠️ Not as specialized | ✅ Very strong |

| Fee-transparency & cost-effectiveness | ✅ Excellent (Digital Nomad World) | ⚠️ Good but may have caveats (Tipalti) | ⚠️ Good for certain flows, but fees can add up (International Money Made Simple) |

| Availability / global reach considerations | ✅ Broad (but check country) | ⚠️ Rapid expansion but still limitations | ✅ Strong for freelancers, but check residence country |

Which should you choose (or combine)?

- If you primarily earn from global clients and need to receive payments easily → Payoneer is a strong candidate.

- If you primarily earn in one currency, travel or live abroad, and want to hold and spend money in multiple currencies → Wise is often the best overall.

- If you travel frequently, want travel-friendly features, ATM access, multi-currency spending, and can accept some trade-offs → Revolut is compelling.

- Often, the best strategy for a digital nomad is to use more than one account: e.g., use Wise as your main multi-currency hub + Payoneer for marketplace income + Revolut for travel spending. Diversification reduces risk (e.g., account freezes, limits) and lets you optimise for cost.

5. How Get Founds Technologies Builds Skill & Community Around This

At Get Founds Technologies we believe building a thriving digital nomad career has two interlocking parts: skills & mindset + systems & infrastructure. Multi-currency banking falls into the systems side. Here’s how our community leverages it:

- In our Nomad Nexus community (WhatsApp subgroups: NomadNest, NomadSync, Nomad Vibes Circle) we host sessions with experts who’ve travelled/freelanced from multiple countries — they share real-world banking setups, pitfalls, regional restrictions.

- We create downloadable checklists: “Opening your first multi-currency account – what questions to ask your provider”, “Checklist after you land in a new country: does your payment flow still work?”.

- We integrate this into our career development tracks for digital nomads: branding + business setup + financial infrastructure. Because you need to look good (branding) + earn (business) + get paid/hold/spend (financial infrastructure).

- We curate peer case studies: members share which accounts they use, why, and how a multi-currency account allowed them to scale internationally — e.g., “I landed a US client, they paid into my EUR account, I held it and converted when rates were better, lived in Bali”.

- We emphasise risk mitigation: Since remote work + travel introduces unique legal/tax/financial exposure, we include modules on how to legally operate as a digital nomad, verify documentation, check residency/bank eligibility and maintain compliance.

By equipping our community with the right bank account choice and the best practices to use it as part of the bigger nomad-career ecosystem, we help people move from “just travelling” to “earning sustainably anywhere in the world”.

6. Actionable Steps for You Right Now

Here’s a short 5-step plan to implement this immediately:

- Audit your income & currency flows

- List where most of your income comes from (USD, EUR, GBP, INR, etc.)

- List in which currency you spend, live, travel

- Identify if you have cross-currency mismatches/frequent conversions

- Pick your primary multi-currency account

- If you expect multi-currency income + frequent travel: open Wise

- If you get paid via marketplaces: open Payoneer

- If you travel a lot and spend abroad: consider Revolut as complement

- Open the account, verify, and receive one payment

- Do the onboarding before your next location change

- Verify your KYC and residency docs ahead of time

- Receive a test payment into the new account to ensure it works

- Set up spending/withdrawal process

- Link your debit card to your travel spending

- Check local ATM networks, fees, currency conversion rates

- Establish when/where you convert held funds to your living-currency

- Join the Nomad Nexus community

- Use Get Founds’ Nomad Nexus to ask questions: “Which account worked for someone living in Vietnam?”, “What issues did someone face when their country changed tax residency?”

- Leverage peer learnings, share your setup and improve.

7. Common Mistakes & How to Avoid Them

- Mistake: One account only — If you rely solely on one bank/fintech and it gets frozen or limits you (e.g., compliance flag), you’re stuck. Solution: Have a backup account.

- Mistake: Ignoring tax/legality — Receiving funds in foreign currency, living in a country you’re not tax resident in, can trigger unexpected tax obligations or legal issues. Always keep documentation and get regional advice.

- Mistake: Converting immediately without strategy — If you receive USD but live in EUR zone, converting right away may lose you value if rates move. Holding currency intelligently is part of the skill set.

- Mistake: Reading only “free” and ignoring hidden fees — E.g., free plan of Revolut may come with exchange mark-ups on weekends, or Payoneer may charge for certain withdrawals. Always check terms.

- Mistake: Using a personal account for business income — Mix of personal + freelance/corporate income can complicate taxes and bank compliance. If you’re building a business presence, choose a proper account labelled “business/freelance”.

Building Your Skills & Career Through Smart Banking

For a digital nomad, a smart banking setup is not a luxury — it’s a career enabler. When you travel, collaborate internationally, build your personal brand and business across borders, you need an account that flows with your lifestyle, your earnings and your future.

By choosing the right multi-currency account (or combination thereof), you remove a key friction point — money. You stop worrying about high conversion costs, awkward client payments, passporting your banking when you switch countries. Instead you can focus on what matters: creating, collaborating, connecting, and growing.

At Get Founds Technologies, our goal is to support you not just to earn, but to scale your remote career, build meaningful networks and live with purpose (the Ikigai of digital nomad life). As part of our community, you’ll access resources, peer-support and expert sessions to master your financial infrastructure, such as multi-currency accounts.

Start today: audit your income flow, open your account, join our Nomad Nexus community and share your setup. Money free-flow across borders is one of the pillars of being a successful nomad — and with the right account you’ll have one strong pillar in place.

Related Post

The Ultimate Beginner’s Guide to Nomad-Friendly Banking Solutions

How to Avoid Hidden Banking Fees While Traveling

How to Budget for a Nomadic Lifestyle Without Overspending

Step-by-Step Guide to Opening a Business Bank Account Abroad